Published February 28, 2025

Navigating Home Affordability: Why Buying Now Could Be Your Best Move

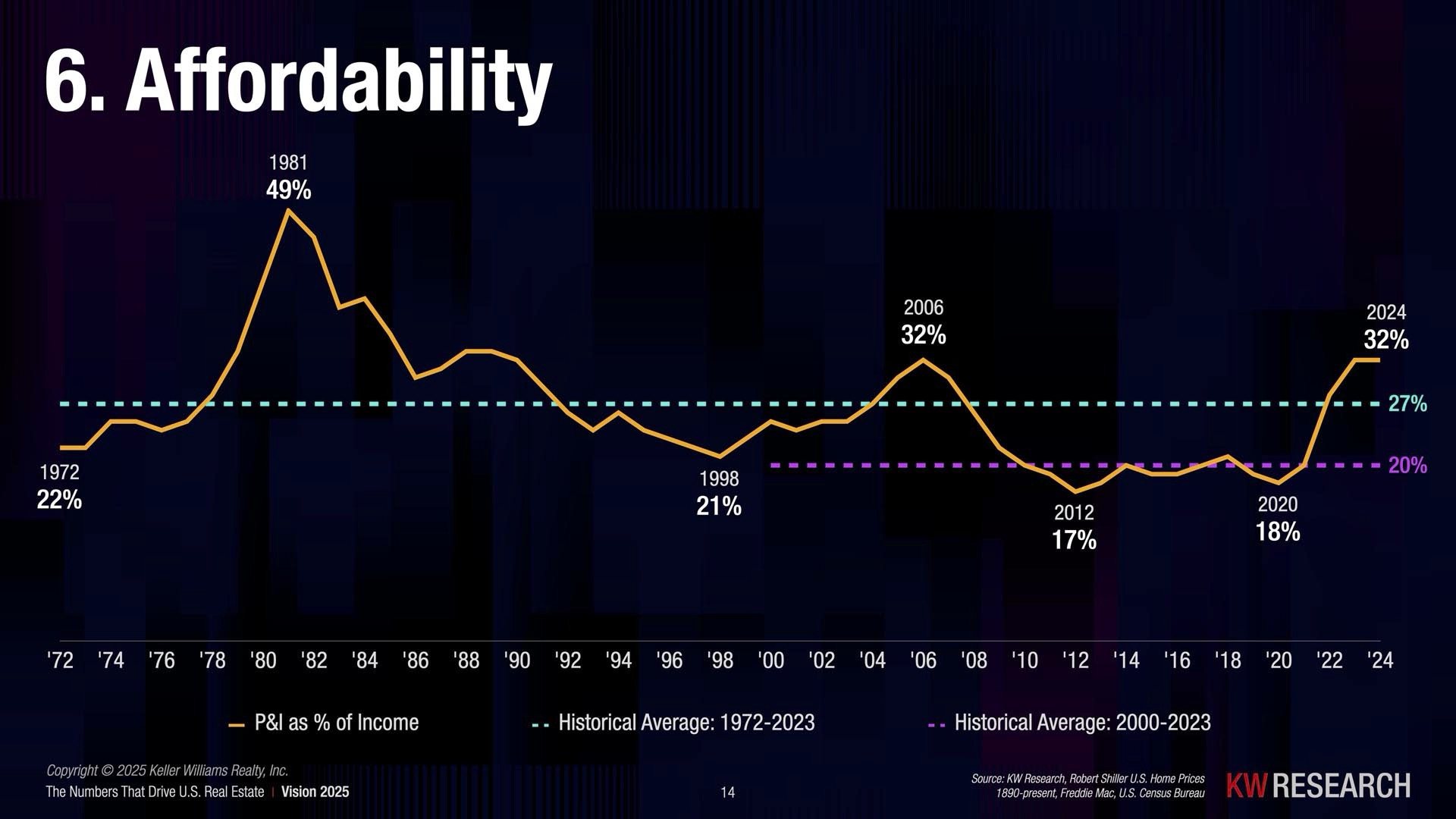

Affordability in the housing market has tightened to levels we haven’t seen in decades. As the graph illustrates, the percentage of income needed to cover principal and interest (P&I) payments has surged to 32%—matching the highs of the 2006 housing peak and nearing the historical highs of the early 1980s. Understandably, this shift has created hesitation among potential buyers. However, history teaches us a crucial lesson: those who take action in uncertain times often benefit the most in the long run.

Even in 1981—when affordability was at its worst, requiring nearly 50% of income for P&I—most homeowners who made the leap then would likely say today that they are glad they did. Why? Because homeownership has historically proven to be one of the greatest tools for wealth accumulation. Those who bought in the 1980s, despite steep interest rates, saw substantial appreciation in property values over time, securing financial stability and generational wealth.

The Economic Shift: A Generational Adjustment

We are now facing a world where money has been cheap to borrow for so long that this adjustment feels jarring. Interest rates were historically low for over a decade, and during the pandemic, savings hit all-time highs. Fast forward to today, and we are witnessing a rapid decline in savings while consumer debt is reaching near-record levels. This isn’t just an affordability crisis—it’s a shift in how we manage money, a generational adjustment where financial habits must evolve.

For many, this means rethinking spending habits. The ease of financing luxury goods, vacations, and short-term indulgences may need to take a backseat in favor of investing in assets—assets that provide security, appreciation, and long-term financial benefits. Historically, real estate has been one of the best-performing assets for building wealth, yet today, hesitation is keeping many from making a move.

The Cost of Waiting: Renting vs. Buying

The biggest mistake many potential homeowners make is assuming that waiting will make things easier. But history suggests otherwise. Consider the following:

Rent Always Increases: Rental prices typically outpace inflation, making renting an ever-growing expense with no return on investment.

Owning Locks in Costs: Even with higher rates, buying a home allows you to lock in a monthly payment and gain equity over time.

Cash-on-Cash Returns in Real Estate Are Unmatched: When factoring in appreciation, tax advantages, and leverage, homeownership remains one of the highest-yielding investments.

While affordability metrics suggest buying a home today requires a larger share of income, this moment may still be the best time to act. As inflation stabilizes and the market adjusts, we could see increased demand drive prices even higher. Homebuyers today are still securing an appreciating asset, whereas those waiting are simply financing someone else’s.

Repositioning Money for Long-Term Wealth

Financial security and wealth accumulation rarely come from choosing what feels easiest in the moment. Those who build lasting wealth prioritize assets over expenses, investments over indulgences, and ownership over temporary convenience.

For many, the home-buying decision isn’t just about today’s affordability metrics—it’s about ensuring a financially stable future. We’ve seen this play out through past cycles. The lesson remains the same: in times of uncertainty, those who act decisively set themselves up for the greatest rewards.

While the market may feel challenging, buying a home today could be one of the most strategic financial decisions you make. The key is shifting the mindset from short-term affordability to long-term opportunity.